Few corners of Europe have lived through a swing as sharp as Greece. In under two decades, the country went from a punishing crash—where GDP collapsed 25% cumulatively (2008–2013) and real estate prices fell 42–45%, to one of the continent's most-watched comebacks, with property prices now 10.8% above their 2008 peak as of Q2 2025.

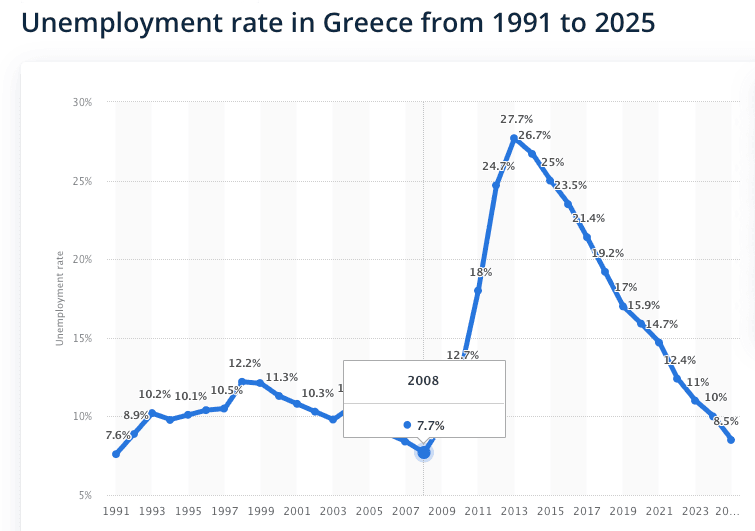

The nation's built environment, which suffered years of declining values, limited liquidity, weak demand, and a threefold jump in unemployment (from 7.1% in 2008 to 28% at its 2013 peak), has transformed into an increasingly attractive destination for international capital, lifestyle buyers, and long-term investors.

This is the complete analysis of how the country's property sector collapsed, stabilised, and ultimately re-emerged as one of Europe's most closely watched asset classes.

source: statista

source: statista

Key Takeaways:

A full-cycle comeback: Values crashed more than 40% from the late-2000s peak to a 2017 low, then rebounded roughly 86% — now sitting above the 2008 pre-crisis high.

Foreign capital led the charge: Tourism, short-term rentals and the Golden Visa drew record overseas buyers, with residency applications hitting 9,407 in 2024.

2024 reforms reset the rules: New tiers (€800K in prime zones, €400K elsewhere, €250K for niche cases) steered money toward quality, long-hold assets.

2026 means mature growth: Prices are rising a healthier 4–7%, above the EU average yet still below the pre-2009 peak in real terms — selectivity now beats timing.

Why Did Greek Real Estate Collapse?

The mid-2000s were heady years. Cheap credit, eurozone optimism and a building spree pushed values to a peak in the late 2000s. Before the global financial crisis, Greece enjoyed years of economic expansion driven by easy access to credit, public spending, and strong domestic consumption. Following the successful hosting of the 2004 Olympic Games, optimism surrounding the country's future encouraged construction activity and homeownership. Then the floor gave way.

However, structural weaknesses were already developing beneath the surface. Government debt continued to grow, productivity lagged behind many European peers, and the economy became increasingly vulnerable to external shocks. The 2008 global financial shock was only the opening blow. When the global financial crisis erupted in 2008, these vulnerabilities quickly became impossible to ignore.

By 2009, concerns surrounding public finances triggered what would become one of the most significant sovereign debt crises in modern European history. Annual home-purchase loan contracts fell from roughly 80,000 before the crisis to no more than 14,000 in the years that followed.

The Beginning of the Downturn

The decline was deep and long. As Greece entered recession, unemployment surged to 28%, youth unemployment hit 59.5% and consumer confidence collapsed. Banks reduced lending activity, making mortgages increasingly difficult to obtain. Domestic purchasers largely withdrew from the market as uncertainty intensified. Transaction volumes fell dramatically while developers struggled to secure financing for new projects.

For nearly a decade, owners watched equity evaporate while transactions stalled and new construction nearly halted.

During this period:

Housing demand contracted significantly.

Construction activity slowed considerably.

Residential prices began a prolonged decline.

Investor sentiment deteriorated.

Credit availability tightened across the economy.

The Deepest Years of the Crisis

The 2009–2010 sovereign-debt crisis turned a slowdown into a free-fall: austerity, double-digit unemployment, the 2015 capital controls (which imposed a €60-per-day ATM limit and closed banks for weeks), and punishing levies such as the ENFIA tax, charging €2.5–16 per square meter for residential spaces, gutted buyer confidence.

Between 2012 and 2017, nominal residential values shed more than 40%, with the sector finally hitting bottom in 2017. Apartments fell by 41% since 2008. Economic output had fallen by approximately 25% compared to pre-crisis levels. Unemployment exceeded 28% at its summer 2013 peak (tripling from 7.1% in 2008), while youth unemployment reached historic highs of 59.5% in Q1 2013.

Residential assets across Athens, Thessaloniki, and many regional cities experienced substantial reductions in value. Distressed sales became increasingly common. New construction nearly disappeared as financing dried up and demand weakened—home construction collapsed by 95%. Numerous projects were halted or postponed indefinitely, with private construction activity declining 42.8% since 2010.

While domestic demand remained subdued, opportunistic international purchasers started identifying value in selected areas. Prime districts of Athens and several island destinations began attracting interest from investors seeking long-term upside potential.

That 2017 trough, however, marked the turning point.

The Turning Point for Greek Real Estate

A major milestone occurred in 2018 when Greece officially exited its final bailout programme, ending 50 months of capital controls that had been imposed in June 2015. Although challenges remained, international confidence began to improve and quickly gathered speed. A surge in tourism—reaching 33 million visitors in 2023, surpassing pre-crisis levels—returning economic stability, and a wave of overseas buyers pulled the country back into growth.

The numbers tell the story. Since the 2017 low, residential values have climbed roughly 86%. From 2019 alone, prices rose about 38%, and some outer Athens suburbs jumped as much as 94% over that stretch. By the third quarter of 2025, nationwide values had not merely recovered—they sat about 7% above the 2008 pre-crisis peak. Apartments specifically have fallen by 41% since 2008 before this recovery, with residential property prices declining 42% (-45.2% in real terms) from the peak year of 2008 before reversing.

The recovery wasn't uniform across the market. Prime Athens districts like Kolonaki, Pagration, and Koukaki saw the strongest gains, with some areas doubling in value from their 2017 bottoms. In outer Athens suburbs including Chalandri, Filothei, and Glyfada, price increases reached 94% from 2019 levels. The island markets—particularly Crete, Mykonos, and Santorini—also attracted significant international investment, with luxury properties in these destinations commanding premium prices from lifestyle buyers.

Economic output had fallen by approximately 25% compared to pre-crisis levels, but by 2018-2019, Greece began posting consistent GDP growth, averaging 2-3% annually. Unemployment, which peaked at 28% in summer 2013, declined steadily to under 10% by 2023, while youth unemployment dropped from its 59.5% peak in Q1 2013. This labor market recovery, combined with the Golden Visa program (requiring €250,000–€500,000 property investment for residency), created sustained demand from foreign investors seeking both lifestyle and investment value in Greece's re-emerging property market.

What Sparked the Wave of Foreign Investment?

Three forces converged: the rebound in tourism, the explosion of short-term rentals, and the Golden Visa residency-by-investment program launched in 2013 at a €250,000 entry point. International appetite proved decisive. Golden Visa applications leapt from 1,993 in 2021 to a record 9,407 in 2024. Foreign capital poured into prime residential and tourism-linked assets 47% of total FDI in 2023 = €2.1 billion, and Attica became one of Europe's most sought-after destinations for overseas buyers.

The programme attracted applicants from:

China

Turkey

Lebanon

Egypt

Israel

United Kingdom

United States

The influx of international capital contributed to rising transaction volumes and helped absorb excess inventory accumulated during the crisis years. Between 2019 and 2023, the recovery accelerated significantly. Despite the temporary disruption caused by the COVID-19 pandemic, the sector demonstrated remarkable resilience.

Values increased across many urban areas, particularly within Athens and its southern coastal districts. Neighbourhoods previously overlooked during the crisis became increasingly attractive to both domestic and international purchasers. Large-scale redevelopment initiatives helped transform key parts of the capital.

Former industrial zones, waterfront districts, and neglected urban areas began attracting substantial investment. Projects such as the redevelopment of the former Ellinikon airport and Piraeus Gate highlighted growing confidence in Greece's long-term prospects. The popularity of platforms such as Airbnb encouraged refurbishment activity throughout Athens and major tourism destinations.

Older buildings were converted into modern accommodation, helping revitalise numerous neighbourhoods.

Where Do Greek House Prices Stand at the Start of 2026?

The picture entering 2026 is one of strength settling into maturity. Drawing on Bank of Greece figures through late 2025:

Nationwide values are about 7% above the 2008 peak and roughly 86% above the 2017 trough.

Attica runs ahead of the national average, around 12.5% above 2008 levels, with southern suburbs, central districts and northern neighbourhoods posting 20–30% gains. Thessaloniki added about 5.7%.

The national average sits near €1,720 per square metre; Athens spans roughly €2,200–€4,100/m², with premium southern suburbs commanding far more.

Annual growth cooled to about 7.7%, down from the double-digit surges of earlier recovery years — a healthy moderation rather than a reversal.

Inflation eased to 2.4% (November 2025), and in the first half of 2025 overseas buyers committed €938 million, about a third of total foreign direct investment.

Demand still outstrips a tight supply, and homes are moving fast — time-on-market in Athens averages under two months.

Greece's Current Economic Situation

Greece's economy has reached a historic normalisation milestone: in May 2027, Greek stocks will return to MSCI's developed markets index, ending its status as the only Eurozone market classified as emerging. This reclassification, announced by Morgan Stanley/MSCI in March 2026, marks the latest step in Greece's post-2009 debt crisis recovery and validates the country's economic stabilisation.

The upgrade broadens Greece's investor base and integrates the Athens Stock Exchange into the Developed Europe single-market index. Supporting this momentum, the MSCI Greece index has returned 38.4% over the year to March 31, 2026. Greece was downgraded to emerging market status in 2013 during the crisis, making this the first market in MSCI history to return to Developed Markets after being moved to Emerging Markets following the euro sovereign debt crisis.

This reclassification comes alongside other recovery indicators: GDP growth of ~2.1% annually, unemployment declining to under 10% (from 28% peak in 2013), tourism contributing €30.2 billion (13% of GDP), and real estate prices sitting 7% above 2008 pre-crisis levels.

From Collapse to Confidence

Greece's journey from the wreckage of the debt crisis to the firm footing of 2026 is a rare full-cycle recovery. The frenzied phase has passed; what remains is a more transparent, mature and investable landscape. For buyers who do their homework on location, legal due diligence and asset quality, the country stays one of Europe's most compelling long-term opportunities — no longer a bargain-basement rebound play, but a market that has earned its place among the continent's serious contenders.