This article examines the conversion of property rights into digital certificates via distributed ledgers, outlining definitions, benefits, mechanisms, risks, EU regulation and principal market participants. The process of converting property ownership into digital shares is reshaping property markets globally, offering new avenues for investment and liquidity. This innovative approach aligns with Greece’s growing interest in modernising its property sector through technology.

Key Takeaways:

Democratized Access: Fractional ownership via digital shares lowers entry barriers, enabling smaller investors to participate in high-value properties.

Streamlined Process: Asset digitization uses decentralized ledgers and smart contracts for instant settlements, cutting costs and administrative delays.

Risk Mitigation: Regulatory gaps and cybersecurity require due diligence; prioritize platforms compliant with frameworks like MICA.

Greek Innovation: Local institutions and EU regulations align to foster secure, transparent property markets through tech-driven solutions.

What is Tokenisation?

Tokenisation refers to dividing physical assets, like property, into smaller digital units. By leveraging distributed ledger systems, these units enable fractional ownership, allowing multiple investors to hold stakes in high-value properties. This method democratises access to markets traditionally dominated by large capital holders. By encoding ownership rights into smart contracts, each digital certificate automates compliance and transfers without traditional intermediaries.

Benefits of Fractional Ownership in Real Estate

Fractionalizing property unlocks liquidity, lowers entry barriers, and enhances market transparency. Tokenised property investments dramatically boost liquidity by enabling 24/7 secondary trading with minimal settlement friction. Investors gain flexibility to trade shares efficiently, while owners benefit from quicker capital raises. Furthermore, programmable contracts streamline processes—such as title transfers and dividend distributions—resulting in cost and time savings.

How Does the Process Function?

A property’s value is assessed and divided into digital shares, recorded securely on a decentralised ledger. Smart contracts encode compliance rules:

Asset Valuation: A property’s market value is appraised by licensed professionals to determine its worth

Digital Division: The asset is split into smaller, tradable units (digital shares), representing fractional ownership

Ledger Registration: Ownership rights and transaction details are recorded on a decentralised, tamper-proof ledger

Platform Integration: Shares are listed on regulated platforms, enabling investors to purchase or trade them securely

Ownership Verification: Investors receive encrypted digital certificates as proof of stake, updated in real time

Automated Compliance: Smart contracts execute terms (e.g., revenue distribution, transfers) without manual intervention

Settlement: Transactions finalise instantly

What Are the Risks of Digitising Assets?

Regulatory uncertainty, cybersecurity threats, and market volatility pose challenges. Jurisdictional disparities in laws may complicate cross-border transactions, while reliance on technology introduces risks like system failures. Custody and cybersecurity challenges necessitate robust key management and insurance to mitigate theft or loss. Investors must prioritise platforms with robust legal and technical safeguards. Regulatory uncertainties—varying national stances on digital assets—can impede cross-border offerings and investor protections.

MICA’s Role in Regulating Property Digitisation

MiCA establishes a unified EU framework for all crypto-entities, covering asset-referenced units and electronic money equivalents, with provisions for issuer authorisation, transparency, disclosure and ongoing supervision. While MiCA does not single out property digitisation, its rules apply to any digital asset representing external value, ensuring legal certainty and investor safeguards across member states. However, it mandates clear disclosures for realty-linked digital shares and requires platforms to comply with anti-money laundering protocols.

Key Institutional Players

BlackRock allocated over $500 million to on-chain treasury and housing initiatives, leveraging digital issuance for institutional-grade instruments

Goldman Sachs Developing tokenised security platforms to offer clients exposure to fractionalised mortgages and property debt

MakerDAO As a leading decentralised stable-coin issuer, it has committed $1 billion toward tokenised US government and property-backed units

Major Custodians and Exchanges Custodial banks and regulated trading venues are integrating digital asset services under DLT-friendly legislation

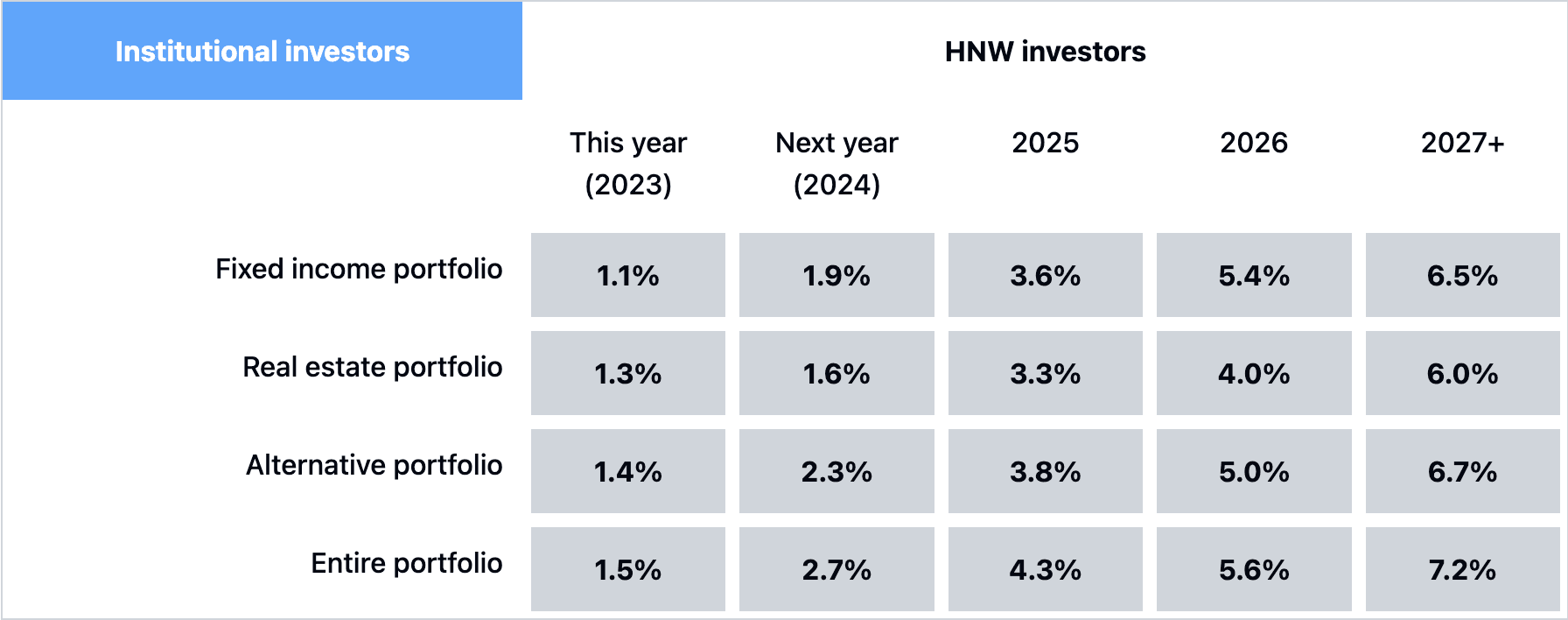

Institutional Investors Surveys indicate institutions plan to allocate 7–9% of portfolios to digital real-world assets by 2027

Source: ey.com

Conclusion

Digital asset issuance for property interests employs distributed ledger technology to transform traditionally illiquid holdings into fractional ownership, enhancing market access and turnover. Key advantages include boosted liquidity, broader investor participation and streamlined transactions, while challenges span cybersecurity, legal clarity and operational complexities. The EU’s Markets in Crypto-Assets Regulation (MiCA) offers a harmonised rule-set for crypto-assets, including asset-backed units, mandating transparency, authorisation and oversight. Major financial institutions—such as BlackRock, Goldman Sachs and leading custodian platforms—are pioneering property digitisation, signalling a shift toward mainstream adoption.

Sources: